No items found.

Subscribe to Monetisation Matters here for in depth articles and actionable insights on Strategy and Monetisation.

Monetisation Matters: Platform, Power, Price

What is a platform business?

Platform businesses are nothing new. There are examples stretching back thousands of years from ancient China, where meiren (matchmakers) would orchestrate marriages and alliances between families, to trade fairs in the County of Champagne1 where participants were carefully selected, mechanisms put in place to enforce contracts and resolve disputes, and credit provided to facilitate trade, all in return for the Count taking a share of the transaction.

Fast forward to today, I am writing this on Google Docs, through Google Chrome, using a Microsoft Windows laptop, sending and receiving data through Notion’s ISP. That’s at least four platforms I’m leveraging to write a single article; a fraction of the true complexity and layers upon layers of platform businesses we are all dependent on.

In an analysis of the Forbes Global 2000 between 1995 and 20152, platform businesses achieved operating margins of 21% vs. 13% for non platform businesses; sales multiples of 5.4 vs. 1.4; and sales growth of 18% vs. 8%. As of January 20243, seven of the top fifteen most valuable public companies in the world based on market capitalisation operate significant platform businesses. For some, such as Microsoft, Meta, VISA and others, platform thinking has been fundamental to how they create value rather than complimentary to a traditional business model.

Despite the success stories, platforms are not guaranteed to become profitable businesses that endure. They have more complex dynamics than traditional businesses and employ what can seem like counterintuitive strategies especially with regards to pricing. The French economist Jean Tirole won a Nobel Prize4 in 2024 partly due to his discoveries into multisided platforms. But before we dig deeper, it's useful to define what exactly we mean by ‘platforms’.

In ‘The Economics of Platforms’ Belleflamme and Peitz define platforms as an “entity that actively manages network effects between economic agents”. Cusumano et al in their book ‘The Business of Platforms’ also require the presence of network effects, splitting platforms into either facilitating transactions and/or acting as a technology foundation for the development of third party innovations.

Given that network effects can be weak, negative, and hard to identify, I prefer a broader definition that does not depend solely on network effects but also includes businesses which act as intermediaries for transactions regardless of the presence or materiality of any network effects.

“A platform acts as an intermediary between participants, managing transactions and/or network effects.”

How do platforms create value?

Platforms aren’t ‘normal’ businesses. They don’t necessarily have a product to sell and don’t always own the relationships with their participants. So how do they create value?

They primarily solve for market failures and frictions where a degree of coordination between people or businesses is required. They facilitate cooperation where it would otherwise fail, reduce search and transaction costs, and provide safe spaces for participants to transact in confidence. I’ve provided some more colour and examples below; the list of benefits is not necessarily exhaustive, but covers the main vectors of value.

Coordination: “I am able to cooperate with others in ways I fundamentally wouldn’t be able to do on my own”

The Interbank Card Association and VISA networks were set up specifically to help acquiring and merchant banks communicate and settle card transactions. Without an intermediary it wouldn’t have been possible for a bank to develop all the relationships it needed to.

Matchmaking and search costs: “I can find what I am looking for”

LinkedIn helps people to connect with that exact individual they’ve been looking for, whilst Uber helps riders to find a car at the right time, and OpenTable to find an available booking for a Friday night. All of these platforms facilitate matchmaking by reducing the cost of search and improving the quality of matches.

Communication: “I can communicate with the participants I’ve found”

Finding what you’re looking for is often just the start of the journey. Platforms such as WhatsApp's fundamental proposition is to facilitate communication, whilst Ebay and Etsy provide the ability to communicate so that buyers and sellers can gain the clarity and confidence they need to transact.

Transaction: “I can complete a transaction efficiently”

Once you’ve found what you’re looking to buy on Etsy, you’ve asked clarifying questions, and gained a level of confidence in the seller, you then need a way to transact efficiently and safely. Platforms are well placed to sit directly in the payment flow, earning the right to a share of transactions. Being able to transact directly on a platform is great for the platform itself but also users, providing a seamless user experience and additional assurances.

Trust: “I can trust this person, or the platform can provide me assurances”

Providing trust plays an important role across many platforms and throughout the lifecycle of engagement between participants from search to eventual transaction. Platforms can provide a level of trust directly through assurances such as eBay’s money back guarantee and Alibaba’s escrow functionality, or deploy features such as identity verification and ratings to weed out bad actors. More generally they determine the governance rules that moderate participant behaviour, acting as a trusted neutral party to resolve disputes.

Managing network effects

A lot of what I’ve covered above depends on network effects, which reflects the impact of adding an additional participant, or an increase in activity on the value of the platform. Network effects will vary in strength and consequence for different groups. A within-group effect reflects the impact of an increase in participants or activity within the same category of participants e.g. members on LinkedIn, whilst a cross-group effect reflects the impact of an increase in participants or activity on a different category of participants e.g. an increase in the number of restaurants available on the OpenTable platform for restaurant goers.

Network effects are not exclusively positive, they are often negative. Traditional businesses sell ‘goods’, platforms often bundle in ‘bads’ intentionally. Advertising is a common ‘bad’ leveraged by platforms. Users create a positive network effect for advertisers by providing their attention, whilst advertisers create a negative network effect for users by supplying advertising they would rather do without. At other times the platform needs to mitigate the impact of damaging network effects it didn’t want. For example, when you search for a ride with Uber, you would rather not have to compete with other riders. They are imposing a negative within-group effect on you. Uber needs to make sure it manages supply and demand appropriately so you don’t get frustrated and switch to a competitor.

One of the key functions of a platform is to manage network effects whether they are positive or negative, intentional or unintentional. How they design their platform, the features they build and governance policies they implement all play an important role. But one of their most powerful levers is pricing. For a traditional business, the prices charged have no impact on the usefulness of the product it supplies. For many platform businesses the prices charged or as we will see subsidies provided have a direct and profound impact on the value and viability of the platform.

Pricing for platforms

Getting the pricing strategy right for a platform is much more important and complex compared to a traditional business. I’m simplifying, but a traditional business really just needs to understand how sensitive customers are to changes in price, whilst a platform needs to worry about how changes in price will impact network effects, and the overall value of the platform.

Key questions for a platform as it designs its pricing strategy:

- How much value does the platform create in aggregate across all groups?

- What’s the minimum value each group requires to participate?

- How sensitive is each group’s participation/activity to changes in price?

The first question deals with whether the platform is addressing enough friction to be viable. The greater the value pie, the more there is to share amongst participating groups. Second, it’s possible that one side of the platform might need an additional incentive to participate, whether that’s being provided something valuable for free or direct payments. Third, each group's participation will be impacted by changes in prices/subsidies, which in turn impacts the value of the platform in aggregate.

Pricing decisions can therefore dynamically alter the value of a platform by impacting participation or activity levels of one or more sides. Getting the balance right will also change over time as the platform proposition develops, or the competitive landscape and negotiating position of participating groups changes. I’ve provided a summary of pricing strategies below for some well known platforms to show how network effects have impacted their approach.

American Express: American Express pays cardholders to use their card either through cashback or rewards. These payments are funded by merchants who pay various fees to AMEX for bringing them customers that tend to spend more than competing card networks, as well as cardholders who roll their credit into a high interest loan. Given that individuals choose which card to use, it makes sense for AMEX to incentivise usage, paid for by the merchant side.

PlayStation/Xbox: New generations of games consoles typically sell below unit cost as they try to build scale (demand side). Sony and Microsoft also provide significant tooling and support to developers for free to help stimulate the development of games (supply side), which is all paid for through royalties generated from game purchases. Getting the price wrong for the console can be really damaging to a new generation's prospects as Sony discovered by overpricing the PS3, and Microsoft found when it hard bundled an expensive camera with the Xbox One.

LinkedIn: LinkedIn’s value is in its scale. The ability to connect with anyone across a broad range of industries has proven to be extremely useful. It offers paid versions with more functionality but that isn’t where it makes its money. The majority is generated through its Talent and Marketing Solutions, both of which require the attention of professionals at scale to recruit from and market to.

The power to grow profitably and endure

Businesses with market power are more fun to work for than those without. It’s what enables them to grow market share and margins vs. competitors and endure through time. The economist, advisor and investor Hamilton Helmer has written more clearly about the properties of market power than anyone else in his book 7 Powers. How power relates to platforms is something he is actively exploring, with some of his early thoughts shared in the Acquired Podcast - well worth a listen.

I’ve summarised his framework below and simplified some of the language, as we can make use of it as we explore what conditions need to hold true for a platform to have a shot at generating power.

Two of the seven powers jump out as being particularly relevant to platform businesses: i) network economies; ii) scale economies.

Network Economies

Hamilton identifies network economies explicitly as a source of power, inherent to many platform businesses. A naive reading of this would be that businesses with network effects enjoy market power, but this isn’t the case. Easy to miss, but it’s reflected in his use of ‘economies’ rather than ‘effects’. Network effects need to be material and difficult for competitors to replicate to generate power. One of the most likely barriers is whether network effects grow in value as the platform scales.

Scale Economies

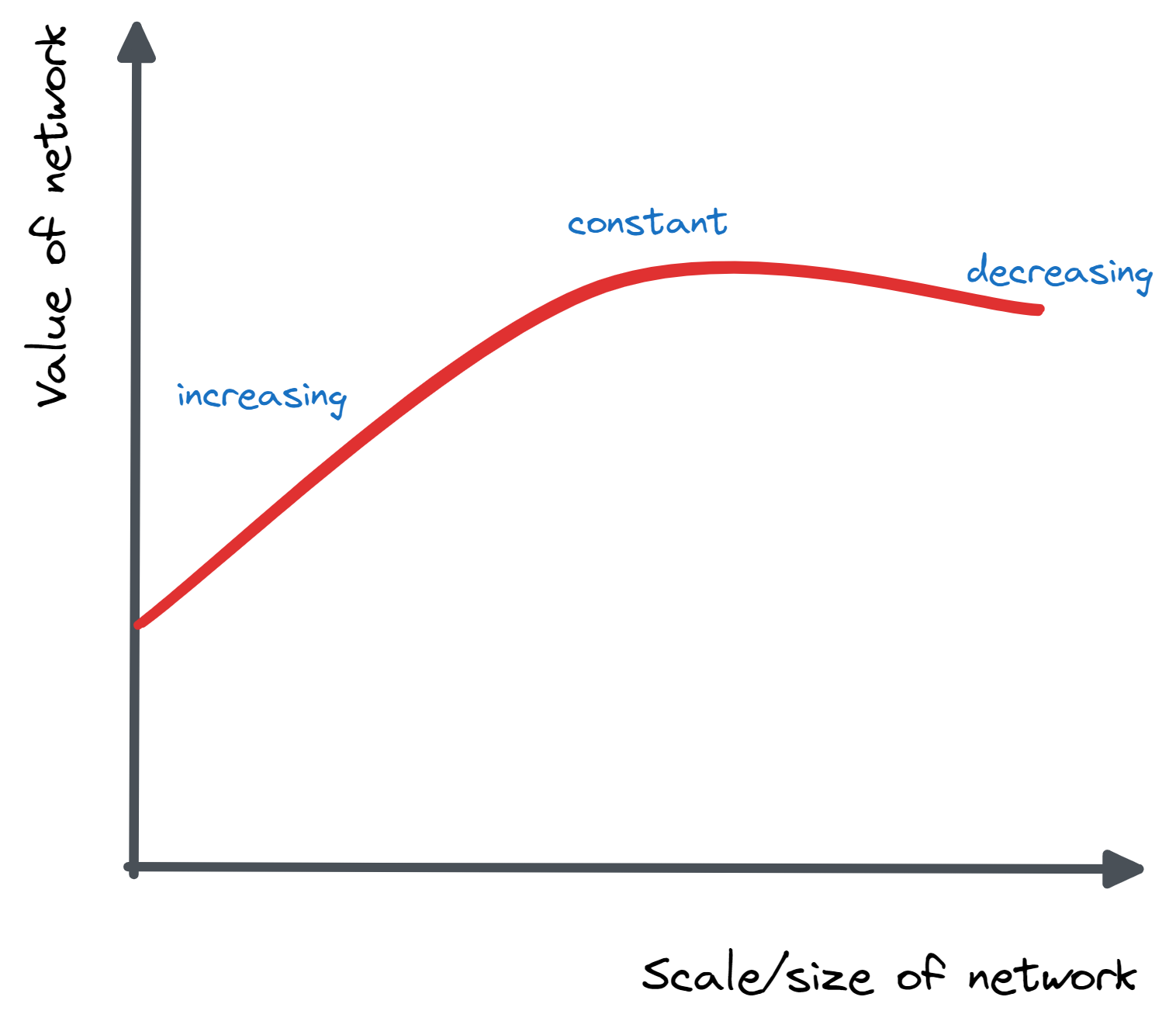

As the scale of a network increases, it’s likely that the quality and efficiency of matching increases and hence so does the value of the network. There may come a point, however, when increasing the size doesn’t have any impact on either value or cost, or it actually starts to have a negative effect. Think of a nightclub you went to too early in the night. It starts off empty and is a pretty boring experience. As it fills up things get more fun for everyone up to a point. Beyond that, it becomes an awful experience as it takes ages to get a drink at the bar and there’s no space for you to show off your terrible moves on the dance floor.

Every platform is different, some are lucky and stay on the ‘increasing’ part of the curve forever, others start to experience constant returns faster than they would like, and if you are really unlucky, they’ve got to deal with damaging decreasing returns or limit the size.

Profiling power

When I set out to write this article I wanted to end with a simple framework that could help categorise platform businesses based on their ability to generate power. That’s proven to be much harder than I imagined. After many iterations I’ve landed on the below which focuses on three things: i) scale economies; ii) nature of network effects; and iii) whether participants are likely to use multiple competing platforms.

Platforms with increasing economies of scale are always going to have more power than those without. Those that benefit from meaningful cross-group network effects are likely to have solved tougher coordination problems than platforms that benefit predominantly from within group effects. Finally, it’s preferable if participants can’t multi-home (participate in multiple networks at the same time).

Just because a platform falls into one of the ‘low power’ buckets doesn’t mean it can't generate market power, rather it’s an indication that it will need to rely on other sources such as switching costs or brand.

I’ve mapped out a few logos below based on where they fit best, however, this does require a degree of judgement. I set a high bar regarding economies of scale; all of these businesses will have enjoyed economies of scale to some extent but what matters is whether that continues over significant scale. I’ve also included the latest operating margins to give some idea of performance.

It’s challenging to find platform’s which benefit from economies of scale and predominantly within-group network effects. It may be that once a platform achieves scale it tends to either get acquired or adds an additional side to the platform to drive monetisation. For example, Facebook’s acquisition of WhatsApp, or LinkedIn’s addition of advertisers and businesses to capitalise on member attention.

Apple and Microsoft are enormous businesses with multiple platform businesses within them. One could make arguments as to why they should move down a bucket, or that different business units should belong in different places. I’ve profiled them as ‘single home’ due to the fact that you only ever really have one operating system installed on your computer, although you are likely to own multiple devices with different operating systems. Whether we push them down a bucket or not, all four logos in that column have significant market power, due in large part to economies of scale.

All the examples I picked on the left enjoy economies of scale and generate impressive margins. The right hand side is a much more mixed picture. Many of these businesses operate at significant scale, but none of them generate meaningful operating margins with ¾ of the examples losing money. A lot is obviously going on under the surface to generate these figures, but they are interesting comparatives nevertheless. An interesting next step is to profile a much larger set of platform businesses to see if any clear patterns emerge.

Summing up

- Platforms act as intermediaries between participants, managing transactions and/or network effects

- They create value by removing friction, helping participants to coordinate and transact safely

- Network effects play an important role, but they are not always positive, and do not necessarily keep improving with scale

- Pricing plays a critical role in managing network effects and ensuring value is shared amongst participants in a way that maintains the value of the platform

- Not all platforms are destined for market power, they require economies of scale at significant scale to generate healthy margins

This has been a far more challenging article to write than I anticipated. Platforms have much more complex dynamics and employ more novel strategies to win than traditional businesses. As software continues to eat the world, it will be interesting to see the business models they disrupt next. B2C has experienced the lion's share of creative destruction so it will be interesting if we see it is more weighted to B2B platforms in future.

.png)

Similiar

Articles

you also may like to read

Similiar

Articles

you also may like to read

.webp)